to estimate the total investment of the project, and compute all the financial indicators of the project.

considers the start up costs, operating costs, revenue projections, sources of financing and profitability analysis.

a. Start-Up Costs: These are the costs incurred in starting up a new business, including “capital goods” such as land, buildings, equipment, etc. The business may have to borrow money from a lending institution to cover these costs.

b. Operating Costs: These are the ongoing costs, such as rent, utilities, and wages that are incurred in the everyday operation of a business. The total should include interest and principle payments on any debt for start-up costs.

.

c. Revenue Projections: How will you price your goods or services? Assess what the estimated monthly revenue will be.

d. Sources of Financing: If your proposed business will need to borrow money from a bank or other lending institution, you may need to research potential lending sources.

e. Profitability Analysis: This is the “bottom line” for the proposed business. Given the costs and revenue analyses above, will your business bring in enough revenue to cover operating expenses? Will it break even, lose money or make a profit? Is there anything you can do to improve the bottom line?

Financial Assumptions

Cost of sales is 60% of the total sales.

Rent expense shall be prorated:

- 1/3 administrative

- 2/3 selling

Tax rate shall be 30%.

Sales increase by 10% in year 2010 and 2011. However, by 2012, it decreases by 4%. Then, in year 2013, it increases again by 1%.

Rent increase by 10% in year 2012.

Net Income shall be prorated:

- J. Acuña - 40%

- C. Fernando – 30%

- M. Abocado – 30%

Drawings shall be 200,000 for J. Acuña while 180,000 for C. Fernando and M. Abocado

Depreciation rate shall be 12.5% per year of the book value.

Financial statements that you need to include in the financial feasibility section:

- Income Statement – shows your revenues, expenses, and profit for a particular period.

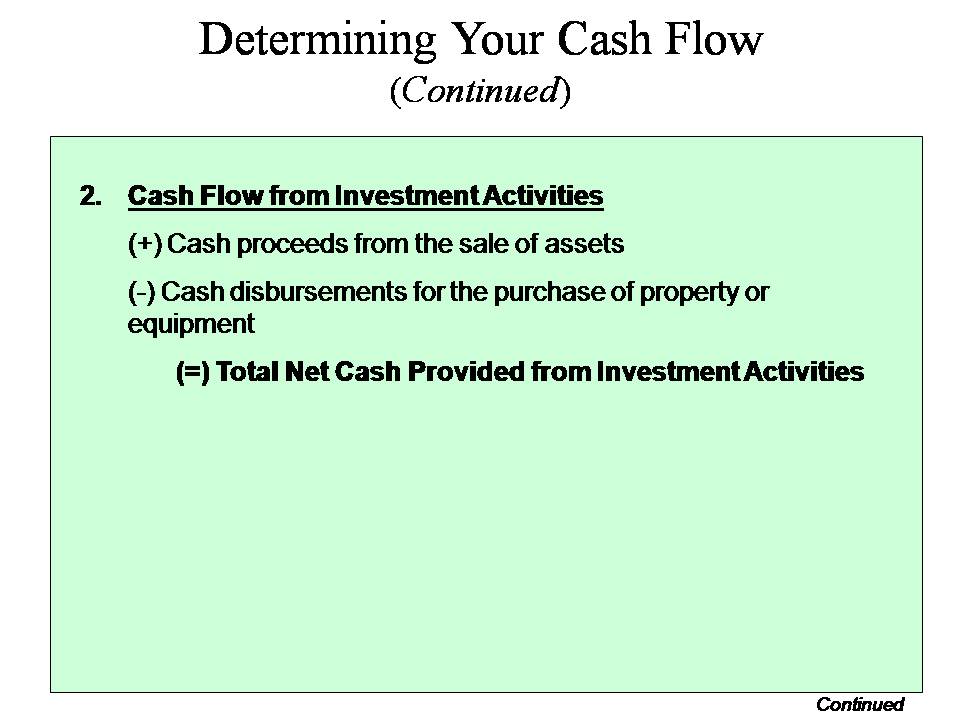

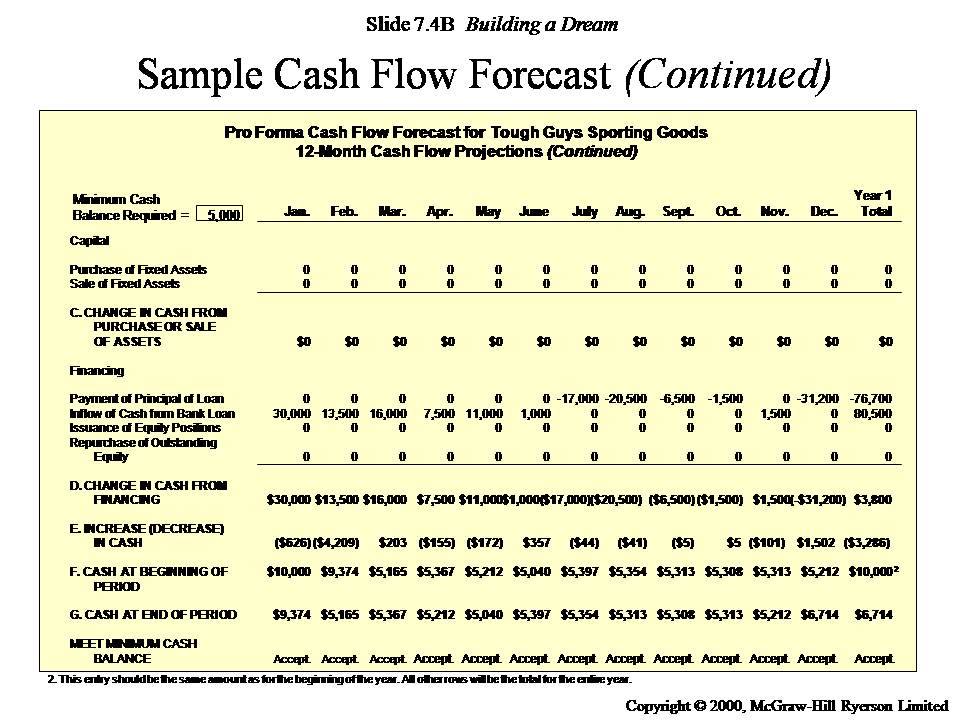

- Cash flow statement – shows how cash has flowed in and out of your business.

- Balance sheet - presents a picture of your business’ net worth at a particular point in time.

- Statement of Changes in Equity – shows the movement in your capital account.

FINANCIAL ANALYSIS

Liquidity Analysis – refers to the company’s ability to pay its short term current liabilities as they fall due.

Current Ratio = Current Assets / Current Liabilities

Quick Ratio = Quick Assets / Current Liabilities

Working Capital Activity Ratios – measures how the firm is effectively using its resources.

Receivables Turnover = Net Credit Sales / Average Receivables

Inventory Turnover = Cost of Goods Sold/ Average Inventory

Debt ratios - are tests of solvency. Solvency refers to the company’s ability to pay all its debts, whether such liabilities are current or non-current. This is somewhat similar to liquidity but this encompasses a longer time horizon.

Working Capital Activity Ratios – measures how the firm is effectively using its resources.

Receivables Turnover = Net Credit Sales / Average Receivables

Inventory Turnover = Cost of Goods Sold/ Average Inventory

Debt ratios - are tests of solvency. Solvency refers to the company’s ability to pay all its debts, whether such liabilities are current or non-current. This is somewhat similar to liquidity but this encompasses a longer time horizon.

No comments:

Post a Comment